Top 10 Banking Industry Challenges — And How You Can Overcome Them

The banking industry is undergoing a radical shift, one driven by new competition from FinTechs, changing business models, mounting regulation and compliance pressures, and disruptive technologies.

The emergence of FinTech/non-bank startups is changing the competitive landscape in financial services, forcing traditional institutions to rethink the way they do business. As data breaches become prevalent and privacy concerns intensify, regulatory and compliance requirements become more restrictive as a result. And, if all of that wasn’t enough, customer demands are evolving as consumers seek round-the-clock personalized service.

These and other banking industry challenges can be resolved by the very technology that’s caused this disruption, but the transition from legacy systems to innovative solutions hasn’t always been an easy one. That said, banks and credit unions need to embrace digital transformation if they wish to not only survive but thrive in the current landscape.

1. Increasing Competition

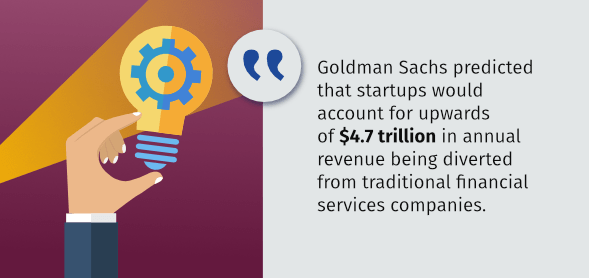

The threat posed by FinTechs, which typically target some of the most profitable areas in financial services, is significant. Goldman Sachs predicted that these startups would account for upwards of $4.7 trillion in annual revenue being diverted from traditional financial services companies.

These new industry entrants are forcing many financial institutions to seek partnerships and/or acquisition opportunities as a stop-gap measure; in fact, Goldman Sachs, themselves, recently made headlines for heavily investing in FinTech. In order to maintain a competitive edge, traditional banks and credit unions must learn from FinTechs, which owe their success to providing a simplified and intuitive customer experience.

2. A Cultural Shift

From artificial intelligence (AI)-enabled wearables that monitor the wearer’s health to smart thermostats that enable you to adjust heating settings from internet-connected devices, technology has become ingrained in our culture — and this extends to the banking industry.

In the digital world, there’s no room for manual processes and systems. Banks and credit unions need to think of technology-based resolutions to banking industry challenges. Therefore, it’s important that financial institutions promote a culture of innovation, in which technology is leveraged to optimize existing processes and procedures for maximum efficiency. This cultural shift toward a technology-first attitude is reflective of the larger industry-wide acceptance of digital transformation.

3. Regulatory Compliance

Regulatory compliance has become one of the most significant banking industry challenges as a direct result of the dramatic increase in regulatory fees relative to earnings and credit losses since the 2008 financial crisis. From Basel’s risk-weighted capital requirements to the Dodd-Frank Act, and from the Financial Account Standards Board’s Current Expected Credit Loss (CECL) to the Allowance for Loan and Lease Losses (ALLL), there are a growing number of regulations that banks and credit unions must comply with; compliance can significantly strain resources and is often dependent on the ability to correlate data from disparate sources.

Major Banking Regulations

| Basel III | Published in 2009, Basel III is a regulatory framework for banks established by the Basel Committee on Banking Supervision. Basel III’s risk-weighted capital requirements dictate the minimum capital adequacy ratio that banks must maintain. |

| Dodd-Frank Act | Passed during the Obama administration, the Dodd-Frank Wall Street Reform and Consumer Protection Act placed regulations on the financial services industry and created programs to prevent predatory lending. |

| CECL | Created by the Financial Accounting Standards Board, the CECL is an accounting standard that requires all institutions that issue a credit to estimate expected losses over the remaining life of the loan, rather than incurred losses. |

| ALLL | The ALLL is a reserve that financial institutions establish based on the estimated credit risk within their assets. |

Faced with severe consequences for non-compliance, banks have incurred additional cost and risk (without a proportional enhancement to risk mitigation) in order to stay up to date on the latest regulatory changes and to implement the controls necessary to satisfy those requirements. Overcoming regulatory compliance challenges requires banks and credit unions to foster a culture of compliance within the organization, as well as implement formal compliance structures and systems.

Technology is a critical component in creating this culture of compliance. Technology that collects and mines data, performs in-depth data analysis, and provides insightful reporting is especially valuable for identifying and minimizing compliance risk. In addition, technology can help standardize processes, ensure procedures are followed correctly and consistently, and enables organizations to keep up with new regulatory/industry policy changes.

4. Changing Business Models

The cost associated with compliance management is just one of many banking industry challenges forcing financial institutions to change the way they do business. The increasing cost of capital combined with sustained low-interest rates, decreasing return on equity, and decreased proprietary trading are all putting pressure on traditional sources of banking profitability. In spite of this, shareholder expectations remain unchanged.

This culmination of factors has led many institutions to create new competitive service offerings, rationalize business lines, and seek sustainable improvements in operational efficiencies to maintain profitability. Failure to adapt to changing demands is not an option; therefore, financial institutions must be structured for agility and be prepared to pivot when necessary.

5. Rising Expectations

Today’s consumer is smarter, savvier, and more informed than ever before and expects a high degree of personalization and convenience out of their banking experience. Changing customer demographics play a major role in these heightened expectations: With each new generation of banking customers comes a more innate understanding of technology and, as a result, an increased expectation of digitized experiences.

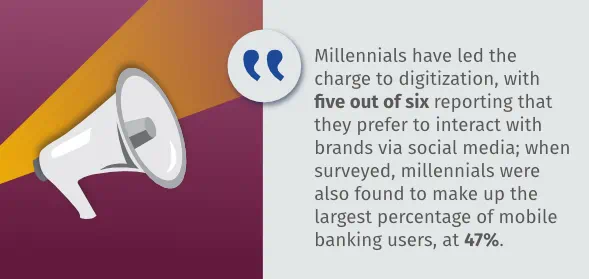

Millennials have led the charge to digitization, with five out of six reporting that they prefer to interact with brands via social media; when surveyed, millennials were also found to make up the largest percentage of mobile banking users, at 47%. Based on this trend, banks can expect future generations, starting with Gen Z, to be even more invested in omnichannel banking and attuned to technology. By comparison, Baby Boomers and older members of Gen X typically value human interaction and prefer to visit physical branch locations.

This presents banks and credit unions with a unique challenge: How can they satisfy older generations and younger generations of banking customers at the same time? The answer to this banking industry challenge is a hybrid banking model that integrates digital experiences into traditional bank branches. Imagine, if you will, a physical branch with a self-service station that displays the most cutting-edge smart devices, which customers can use to access their bank’s knowledge base. Should a customer require additional assistance, they can use one of these devices to schedule an appointment with one of the branch’s financial advisors; during the appointment, the advisor will answer any of the customer’s questions, as well as set them up with a mobile AI assistant that can provide them with additional recommendations based on their behavior. It might sound too good to be true, but the branch of the future already exists, and it’s helping banks and credit unions meet and exceed rising customer expectations.

Investor expectations must be accounted for, as well. Annual profits are a major concern — after all, stakeholders need to know that they’ll receive a return on their investment or equity and, in order for that to happen, banks need to actually turn a profit. This ties back into customer expectations because, in an increasingly constituent-centric world, satisfied customers are the key to sustained business success — so, the happier your customers are, the happier your investors will be.

The Time is Now: Digital Transformation in Financial Services

Financial services organizations are at a transformational tipping point. Faced with fierce market pressures throughout the industry technology transformation is no longer merely a competitive advantage, but an absolute necessity. Our experts break down the six key areas to focus your digital transformation strategy.

Get the free ebook6. Customer Retention

Financial services customers expect personalized and meaningful experiences through simple and intuitive interfaces on any device, anywhere, and at any time. Although customer experience can be hard to quantify, customer turnover is tangible and customer loyalty is quickly becoming an endangered concept. Customer loyalty is a product of rich client relationships that begin with knowing the customer and their expectations, as well as implementing an ongoing client-centric approach.

In an Accenture Financial Services global study of nearly 33,000 banking customers spanning 18 markets, 49% of respondents indicated that customer service drives loyalty. By knowing the customer and engaging with them accordingly, financial institutions can optimize interactions that result in increased customer satisfaction and wallet share, and a subsequent decrease in customer churn

Bots are one new tool financial organizations can use to deliver superior customer service. Bots are a helpful way to increase customer engagement without incurring additional costs, and studies show that the majority of consumers prefer virtual assistance for timely issue resolution. As the first line of customer interaction, bots can engage customers naturally, conversationally, and contextually, thereby improving resolution time and customer satisfaction. Using sentiment analysis, bots are also able to gather information through dialogue, while understanding context through the recognition of emotional cues. With this information, they can quickly evaluate, escalate, and route complex issues to humans for resolution.

7. Outdated Mobile Experiences

These days, every bank or credit union has its own branded mobile application — however, just because an organization has a mobile banking strategy doesn’t mean that it’s being leveraged as effectively as possible. A bank’s mobile experience needs to be fast, easy to use, fully-featured (think live chat, voice-enabled digital assistance, and the like), secure, and regularly updated in order to keep customers satisfied. Some banks have even started to reimagine what a banking app could be by introducing mobile payment functionality that enables customers to treat their smartphones like secure digital wallets and instantly transfer money to family and friends.

8. Security Breaches

With a series of high-profile breaches over the past few years, security is one of the leading banking industry challenges, as well as a major concern for bank and credit union customers. Financial institutions must invest in the latest technology-driven security measures to keep sensitive customers safe, such as:

- Address Verification Service (AVS): AVS “checks the billing address submitted by the card user with the cardholder’s billing address on record at the issuing bank” in order to identify suspicious transactions and prevent fraudulent activity.

- End-to-End Encryption (E2EE): E2EE “is a method of secure communication that prevents third-parties from accessing data while it’s transferred from one end system or device to another.” E2EE uses cryptographic keys, which are stored at each endpoint, to encrypt and decrypt private messages. Banks and credit unions can use E2EE to secure mobile transactions and other online payments so that funds are securely transferred from one account to another, or from a customer to a retailer.

- Authentication:

- Biometric authentication “is a security process that relies on the unique biological characteristics of an individual to verify that he is who he says he is. Biometric authentication systems compare a biometric data capture to stored, confirmed authentic data in a database.” Common forms of biometric authentication include voice and facial recognition and iris and fingerprint scans. Banks and credit unions can use biometric authentication in place of PINs, as it’s more difficult to replicate and, therefore, more secure.

- Location-based authentication (sometimes referred to as geolocation identification) “is a special procedure to prove an individual’s identity and authenticity on appearance simply by detecting its presence at a distinct location.” Banks can use location-based authentication in conjunction with mobile banking to prevent fraud by either sending out a push notification to a customer’s mobile device authorizing a transaction, or by triangulating the customer’s location to determine whether they’re in the same location in which the transaction is taking place.

- Out-of-band authentication (OOBA) refers to “a process where authentication requires two different signals from two different networks or channels… [By] using two different channels, authentication systems can guard against fraudulent users that may only have access to one of these channels.” Banks can use OOBA to generate a one-time security code, which the customer receives via automated voice call, SMS text message, or email; the customer then enters that security code to access their account, thereby verifying their identity.

- Risk-based authentication (RBA) — also known as adaptive authentication or step-up authentication — “is a method of applying varying levels of stringency to authentication processes based on the likelihood that access to a given system could result in its being compromised.” RBA enables banks and credit unions to tailor their security measures to the risk level of each customer transaction.

9. Antiquated Applications

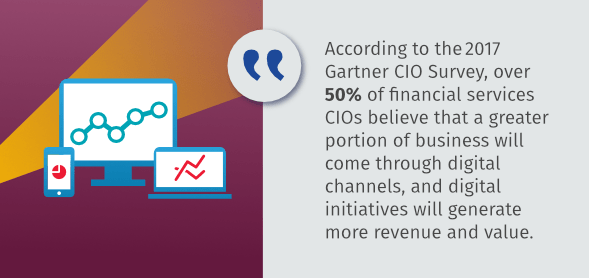

According to the 2017 Gartner CIO Survey, over 50% of financial services CIOs believe that a greater portion of business will come through digital channels, and digital initiatives will generate more revenue and value.

However, organizations using antiquated business management applications or siloed systems will be unable to keep up with this increasingly digital-first world. Without a solid, forward-thinking technological foundation, organizations will miss out on critical business evolution. In other words, digital transformation is not just a good idea — it’s become imperative for survival.

While technologies such as blockchain may still be too immature to realize significant returns from their implementation in the near future, technologies like cloud computing, AI, and bots all offer significant advantages for institutions looking to reduce costs while improving customer satisfaction and growing wallet share.

Cloud computing via software as a service and platform as a service solutions enable firms previously burdened with disparate legacy systems to simplify and standardize IT estates. In doing so, banks and credit unions are able to reduce costs and improve data analytics, all while leveraging leading-edge technologies. AI offers a significant competitive advantage by providing deep insights into customer behaviors and needs, giving financial institutions the ability to sell the right product at the right time to the right customer. Additionally, AI can provide key organizational insights required to identify operational opportunities and maintain agility.

10. Continuous Innovation

Sustainable success in business requires insight, agility, rich client relationships, and continuous innovation. Benchmarking effective practices throughout the industry can provide valuable insight, helping banks and credit unions stay competitive. However, benchmarking alone only enables institutions to keep up with the pack — it rarely leads to innovation. As the cliché goes, businesses must benchmark to survive, but innovate to thrive; innovation is a key differentiator that separates the wheat from the chaff.

Innovation stems from insights, and insights are discovered through customer interactions and continuous organizational analysis. Insights without action, however, are impotent — it’s vital that financial institutions be prepared to pivot when necessary to address market demands while improving upon the customer experience.

Financial service organizations leveraging the latest business technology, particularly around cloud applications, have a key advantage in the digital transformation race: They can innovate faster. The power of cloud technology is its agility and scalability. Without system hardware limiting flexibility, cloud technology enables systems to evolve along with your business.

How Hitachi Solutions Can Help

With so many banking industry challenges to contend with, charting a clear path forward can seem like an overwhelming task — but with the right team to support your efforts, digital transformation is attainable. The financial services team at Hitachi Solutions has been helping banks and credit unions unlock digital experiences through the power of the Microsoft platform since 2004. With a wide variety of products and services tailored to the financial services industry, such as Engage for Banking and Retail Banking Sales Insights, we’re familiar with the unique issues financial institutions face and have developed the technology to resolve them.

From data science expertise to business intelligence, AI, and beyond, Hitachi Solutions is here to help your organization tackle banking industry challenges and embrace digital transformation.